Changing UK Pension Landscape and Brexit

In this blog, Imperius Wealth’s Gerard Frew (Chartered Financial Planner) examines the changes to UK Pensions over the last few years and how the changes are affecting people with UK Pensions.

Top points to consider:

- Legislative changes to UK Pensions

- On the 6th of April 2015 the UK Government passed radical legislation enabling everyone with a Defined Contribution pension scheme to be able to access the benefits of their scheme from the age of 55 on a flexible basis.

- The key word here is flexible, basically this meant that you could, in effect, withdraw the full value of your pension in one transaction if that was your intention. This was a huge development as it had the effect of changing the responsibility from the government to the individual and empowering them to make their own decisions in regard to their retirement.

Finally, they trusted us, the public, to be responsible enough to look after our own money! However, I had my doubts at the time as to whether the government was doing this to be kind or in the hope that it would generate a large, quick tax take as people suddenly realised that they could get their hands on money that had previously been off limits.

At the time there was concern from the advice community that people would not take advice, and this would mean people would delve into their hard earned pension funds and potentially sleep-walk into a huge tax bill!

5 key points

- UK Changed Pension rules in 2015.

- New flexible access options.

- Improved lower cost options.

- Brexit creates complexity for EU residents.

- Avoid unnecessary UK tax

New UK Pension Freedom & Options

With Pensions Freedom, the ability to move your Defined Benefit Pension Scheme to a flexible personal pension or defined contribution scheme also became more attractive in the eyes of the public. This set in motion a series of events that would see billions of pounds move from “gold-plated” or secure annual pensions into more flexible, easier to access defined contribution schemes. Most people weren’t aware that the small annual pension they had from their DB scheme was worth potentially hundreds of thousands of pounds and sent the DB transfer market into a frenzy. Here is a recent article from the FT covering the subject.

The only problem with this was that, as is mostly always the case, a new law is passed and then we think of the consequences that this causes, people wrongly advised, huge fees to transfer and a number of questionable investment schemes, rather than thinking about it before the law is passed!

The FCA then tried to step in, once the damage had been largely done, and decided to close the stable door, long after the horse had bolted. With recent well publicised events, such as The British Steel pensions debacle.

Changing rules for UK Defined Benefit / Final Salary Pensions

The FCA brought out tougher new rules with regard to the transfer of Defined Benefit Pensions and also increased the compensation limit to £350,000, virtually overnight, meaning that transferring your defined benefit scheme not only became more difficult but finding an adviser with the right qualifications, licenses and Professional Indemnity cover to do the transfer became even harder. This in effect has been causing the market to shrink as more and more advisers have decided that it is just too much of a risk or indeed the FCA have deemed the advisers too much of a risk and “assisted” them in making their decision.

The impact of Brexit on UK Pensions

So with regard to Brexit, how will this effect pensions in the UK? The short answers is, if you are based in the UK and never go abroad, then over the next few months and years it is likely that prices will rise and your pension is going to be a little more stretched than previously in retirement. If you like to go on foreign holidays, then it’s likely that your pound won’t go as far as it did pre Brexit, effectively making you poorer. The current COVID 19 virus is effectively putting a temporary stop to most travel anyway, however we expect things to get back to some sense of normality next year.

Resident in Ireland or EU

If you have moved away from the UK and are currently living in Ireland or Portugal for example, or anywhere else in the Eurozone for that matter then your pension is going to be worth less in spending terms in the event of a weaker sterling, especially if you decide to keep your pension in the UK and draw the monies in sterling. This causes another risk in addition to investment risk and inflation risk, CURRENCY RISK. Sometimes it is worth considering a Qualified Overseas Pension Scheme (QROPS) or an International SIPP with currency options to negate currency risks to some degree.

With regard to the current COVID 19 financial package the UK government has outlined, this will, like most other countries have a long term effect on national debt figures, resulting in higher tax bills to come in the future and may also have a long lasting effect on sterling.

Important to review your options

It is always good to review your retirement strategy on an annual basis, especially when you are over 50 and the magical age of 55 approaches, as with all the changes in the current pensions landscape it’s better to know both what you want to do and what you can afford to do. A good adviser will and should always give you the unvarnished truth and help you plan so that retirement is not just simply arrived at but carefully thought out and planned for.

The top reasons for transferring a pension are as follows;

- Flexibility to access your funds as and when you wish from age 55

- Ability to pass on a legacy to your family

- Ill health or reduced life expectancy

- Paying down debt in retirement

- Left the UK and wish to transfer to an equivalent overseas scheme.

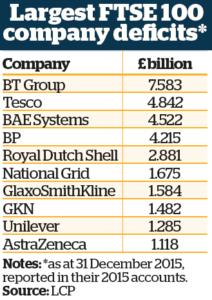

Some of the companies that offered this type of salary based scheme are listed below, note that a lot of these firms no longer offer this benefit to new members (due to the high cost of doing so), this is not a complete list, just an example.

RBS, HBOS, HSBC, Barclays, Vodafone, BP, Most Local Authorities, USS, Unilever, Royal Dutch Shell, Tesco, British Telecom, Teachers Pension, Imperial Chemicals, BT, see below for some of the deficits in these schemes as at 31st December 2015.

If you worked for a large, FTSE 100 company, local authority or government based role then you are likely to have a final salary/defined benefit pension scheme from either some part or all of your service there.

If you are lucky enough to have one of the last remaining Defined Benefit/Final Salary Pension Schemes, make sure you seek out appropriate advice when assessing your options.

You should be aware that a transfer is not always right for you and this decision should be arrived at after sourcing advice from a qualified expert in this field, a small annual defined benefit pension can be worth a lot of money in terms of the transfer value, something that needs to be looked at very carefully before cashing in.

At Imperius Wealth, we assess your options and make sure you make the decision that’s appropriate for you and your family. Contact us today to discuss your options and for a free no obligation discussion on the subject.