Standard Fund Threshold (‘SFT’) – 5 items to consider if your Pension is approaching the Irish SFT of €2 million

Standard Fund Threshold (‘SFT’)

June 5, 2024

The Irish Revenue SFT is currently at €2 million, this means that an individual can tax effectively build a pension fund in their working lifetime (both private and public sector up to this limit). If their fund is greater than €2m then they are liable to Irish Revenue at a chargeable excess tax rate of 40% on every Euro accumulated in their pension fund over this limit

The real Standard Fund Threshold:

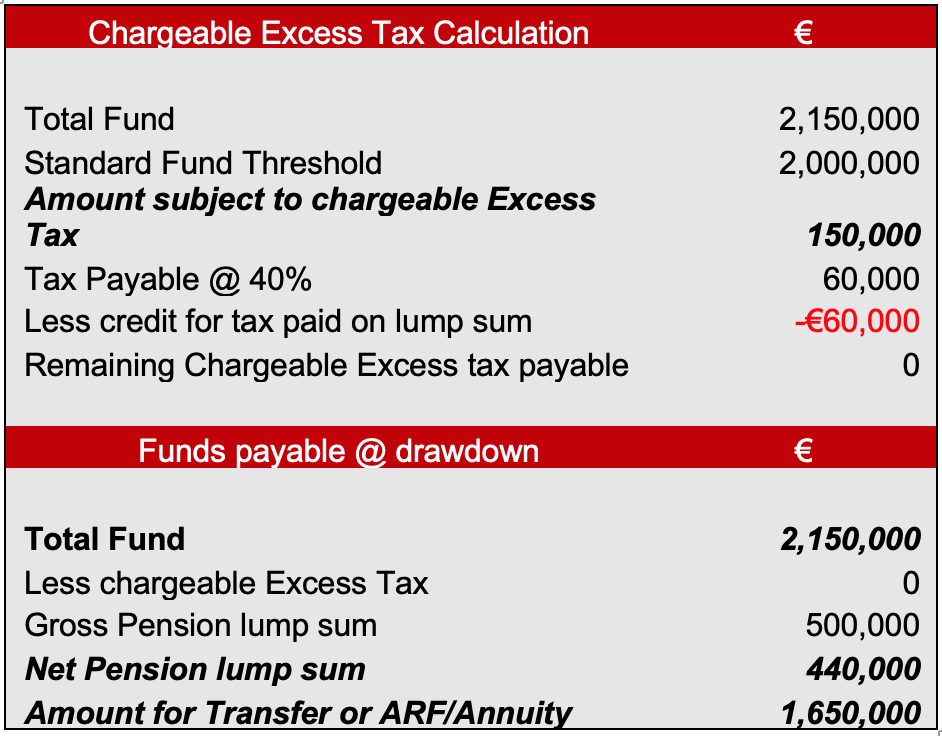

It is however possible for those with Defined Contribution pensions to fund for a higher amount without incurring this chargeable excess tax rate. A DC Pension holder can grow a fund to €2.15m and avoid paying any excess tax.

How is this achieved?

In the example below, an individual builds their fund to €2.15m, he/she takes the maximum limit of tax free and taxable funds of €500,000 (pays 0% tax on €200k and 20% on €300k). The €60,000 lump sum tax paid is applied as a credit to offset the chargeable excess tax.

How easily can a pension fund accumulate over time and potentially breach this SFT limit?

Source: Standard Life 02/2023

Assumptions

- In our example the individual is 50 years of age and has a DC pension of €1.6m

- The fund grows at a conservative rate of 3.0% p.a. net of fees.

- There are no regular monthly/ annual contributions to the fund.

Comments.

- Our example shows that with a conservative 3% growth rate, the SFT limit is reached within 10 years.

- By age 60, our client’s fund has grown to €2.15m from €1.6m.

- For an individual with a €1.7m pension at age 50, this is expected to accumulate to €2.28m at 58 yrs. giving them a tax headache with excess tax payable @ 40%.

Five tips for consideration to help avoid this punitive/unnecessary tax?

Anyone that has concerns that their existing pension may reach or breach the SFT over the next few years, should arrange a meeting with their Financial Advisor to take action that can reduce any unnecessary tax liabilities from arising. These advice tips include:

- Cease any regular contributions or AVC top ups: Although pension contributions are tax effective and receive tax relief at the marginal rate, that benefit is negated if any contributions lead to an excess tax charge of 40%. If there is Income drawdown on the Penson fund this is taxable at 52%, to avoid any double taxation a pension holder is advised to cease any personal or company contributions.

- Reduce the risk profile in the Pension Investment Strategy: A lower allocation to higher risk assets (Equities and Property) towards lower yielding risk assets (Bonds and Cash) would be expected to slow down the return performance of the pension fund while at the same time reducing the risk profile (known as ‘Lifestyling’) and a strategy that many asset managers utilize in the 5-10 years before the holder’s normal retirement age. In certain circumstances moving all an individual’s pension fund to cash can be advisable to manage up to the SFT.

- Transfer Irish Pension Benefits to an International Pension Arrangement (IORPS II); Most Occupational and Executive Pensions schemes are eligible for a transfer to a similar arrangement in the EU under IORPS II. Malta has acted very successfully as a hub for international pension transfers. For example, an individual aged 50 with a €1.5 million pension could transfer their pension to a Maltese trustee arrangement, they are not constrained by the Irish SFT and can continue to grow their pension beyond the SFT limit without any penalties. There is greater flexibility with a Maltese Pension trust on drawdowns in retirement. If the individual remains in Ireland, they can get the 25% tax free lump sum up benefit to the €200,000 individual limit, however if they are non-resident Ireland, they could potentially get an increased tax-free lump sum of 30%. International Pension transfers is a specialist advice piece and requires detailed planning ahead of any potential move overseas.

- Consider Accessing Pensions Benefits early– Some Irish Pension arrangements allow access early from age 50. If an individual is close to the SFT limit, it may be advisable to take benefits on early retirement before the accumulated pension benefits goes through the SFT limit. The benefit is that they get access to their tax-free lump sum and taxable cash early, while investing the remaining 75% in an ARF arrangement. The SFT limit, does not apply to the value of the ARF assets, the funds can roll up tax free, while the imputed distribution does not start until aged 61 years.

- How to calculate the value of a Defined Benefit Pension: For individuals who have a combination of ‘DC’ Plans and ‘DB’ pension (e.g. HSE Consultants) assessing how close their combined values are to the SFT is more complex and requires bespoke analysis. As a guide, DB Pension benefits are split into ‘pre-2014’ and ‘post-2014’ and then multiplied by a Revenue age related factor, to arrive at an estimated Transfer Value.

If what you have read resonates with you, should you have any questions on this or any other aspects relating to steps to take if approaching the Standard Fund Threshold, please get in touch to arrange a consultation with one of our financial experts here at Imperius Wealth and we will be happy to guide you through the possibilities.

Subscribe to the latest news and insights from Imperius Wealth

imperiuswealth.com needs the contact information you provide to us to contact you about our products and services. You may unsubscribe from these communications at anytime. For information on how to unsubscribe, as well as our privacy practices and commitment to protecting your privacy, check out our Privacy Policy.