Pan European Pensions Product In Ireland

As Europeans, Irish residents will soon be able to benefit from a new EU wide retirement saving plan known as a Pan European Pension Product.

The PEPP Regulation was published on 25 July 2019 and in August 2020, the European Insurance and Occupational Pensions Authority (EIOPA) delivered to the European Commission the draft Regulatory Standards and advice on the delivery of the Pan European Pension Product (PEPP).

The European Commission has now approved EIOPA’s Regulatory Technical Standards per 18 December 2020 so The first PEPPs are expected to enter the market by the beginning of 2022.

So, what is a Pan-European Personal Pension Product or PEPP?

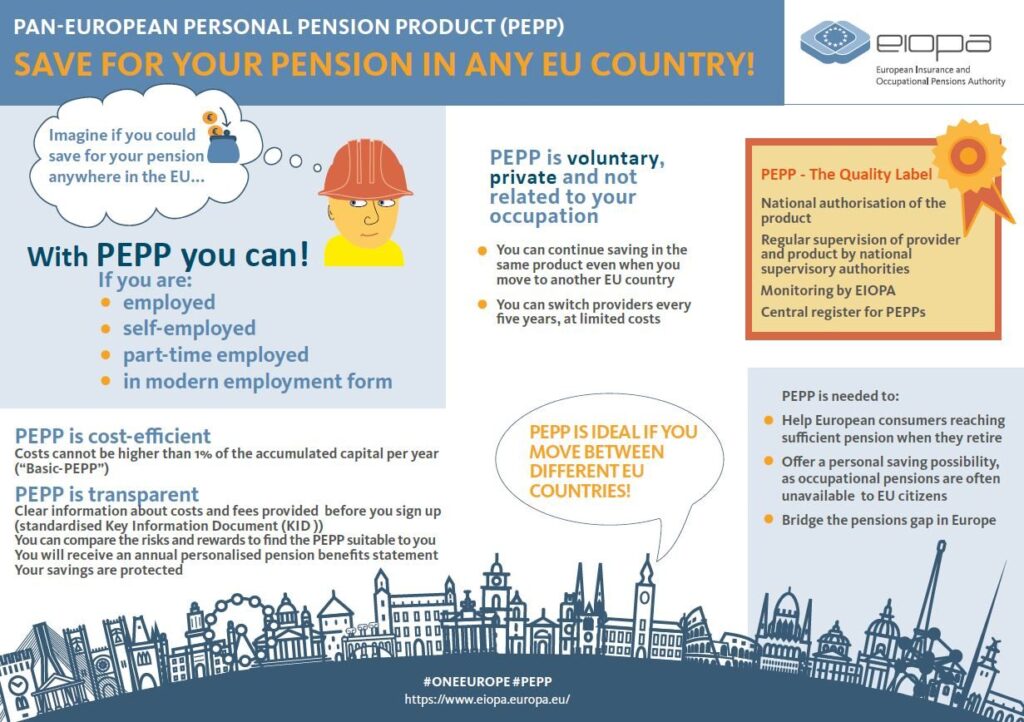

A Pan-European Personal Pension Product or PEPP, is a voluntary pensions product, complementary to state-based Pensions and occupational pensions.

A Pan-European Personal Pension Product is a long-term, individual, non-occupational (i.e. private, apart from a professional status) personal pension product, subscribed to voluntarily by a so-called ‘PEPP saver’ in view of providing income on retirement.

A PEPP will be financed by contributions paid to an (individual) PEPP account, either made by the PEPP saver, or by third parties on the PEPP saver’s behalf. Although PEPPs will not be linked to an employment relationship, employers as third parties, may be able to pay contributions to a PEPP on their behalf or for the benefit of the employee, self-employed person or another individual.

PEPPs are generally not aimed at replacing the existing public and occupational pension systems, but they merely serve as a ‘complementary’ pension product to the present national public and private pension schemes.

The PEPP-Regulation lays down the standardisation of the key PEPP features, the most important of which are:

- Costs – Full transparency on the product, including costs and fees.

- Communication – over the life of the product, a PEPP saver shall be provided, annually, with a standardised Pension Benefit Statement.

- Mandatory Advice – Consumers will also benefit from full mandatory advice, both prior to purchasing a product, as well as just before retirement.

- Portability – One of PEPP’s main characteristics for purposes of creating the single European pension market, is the so-called ‘portability’ feature provided for in the PEPP-Regulation. PEPP savers shall have the right to use a portability service when changing their residence to another Member State by opening a PEPP sub-account with the same PEPP provider in their new Member State of residence or, consumers will be given the possibility to switch provider, free of charge and without delay, or to continue to contribute to the PEPP on the previous country residence.

- Switching right – a PEPP saver will have the right to switch PEPP providers at a capped cost after a minimum of five years however a PEPP provider may allow PEPP savers to switch PEPP providers more frequently.

When using the portability service, PEPP savers are entitled to retain all advantages and incentives granted by the PEPP provider and connected with continuous investment in their PEPP.

As far as tax is concerned, the European Commission encouraged the EU Member States to grant the same tax treatment to PEPP as to similar existing national products to ensure that the PEPP is successfully introduced, irrespective of whether a PEPP is provided by a provider from another Member States or would not satisfy one or more criteria under national tax law to obtain tax relief.

The very recent Report of the Interdepartmental Pensions Reform & Taxation Group 2020 indicates that Ireland intend on using a reformed version of the Personal Retirement Savings Accounts as the Pan European Pension Product. This report advises that “Such an approach would not be without challenge as the PEPP Regulation has a number of specific requirements that do not apply to, or are not comparable to, the PRSA”.

The portability of a Personal Retirement Savings Account will be an issue that must be addressed as the current PRSA legislation and how the transfer of PRSAs overseas is written into the Taxes Consolidation Act 1997 (Section 787G) will be in contravention with the portability characteristic of the Pan European Pension Product. Please see our blog on Transferring a Personal Retirement Savings Account overseas.

A PEPP will be available to anyone having their residence in one of the European Member States wishing to save for their pension, regardless of their status (employees, self-employed, students, part-time or un-employed can all subscribe to a PEPP) and whatever their nationality, as also ‘third country individuals’ will be able to save in a PEPP.

It is expected that PEPP will be of particular interest to ‘mobile citizens’, or those who are planning on moving to other European countries.

If you have retirement savings in Ireland and are resident in another country, please get in touch with Johnny Mulholland or any of the team in Imperius Wealth Ltd and we would be happy to discuss the impact and opportunities of the PEPP Regulation or International Pension Transfers.