QUIETER MONTH FOR GLOBAL ASSETS DESPITE U.S. BANKING SECTOR & DEBT CEILING JITTERS

Stock markets experienced their second consecutive positive month, not withstanding a further bank failure and the ongoing uncertainty about when central banks will pause and then begin reducing interest rates.

The S&P 500 gained 1.5% during April, while the Nasdaq moved sideways. The Euro Stoxx 50 added 1%, while the FTSE 100 and Nikkei indices increased 3.1% and 3.9% respectively. China’s CSI 300 retreated 0.5%, with mixed economic data suggesting the economic bounce-back may have run its course. Commodity markets were also weak, the oil price declined for the fourth consecutive month and bond markets were mixed.

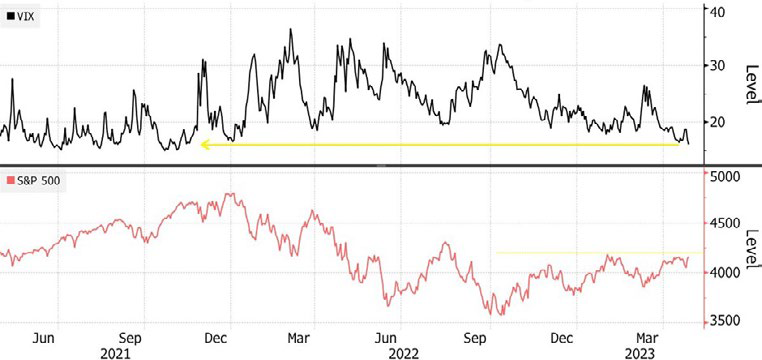

Concerns of US investors were calmed through the first half of the earnings season, with 80% of the S&P 500 companies that have reported earnings so far managing to beat (modest) expectations. The solid earnings saw the CBOE Volatility Index, Wall Street’s ‘fear gauge’, decline below 16 for the first time since November 2021.

But this may be the calm before the storm. There are concerns that markets are pricing in an overly optimistic outlook based on expectations that interest rates will be brought down at some stage this year. This is contrary to Fed guidance that indicates

this may not be the case because inflation remains sticky – and still well out of reach of its 2% target.

"SOLID EARNINGS SAW THE CBOE VOLATILITY INDEX, WALL STREET’S ‘FEAR GAUGE’, DECLINE BELOW 16 FOR THE FIRST TIME SINCE NOVEMBER 2021"

Market calm masks battle underneath VIX falls to fresh

low while S&P 500 faces resistance at 4,200

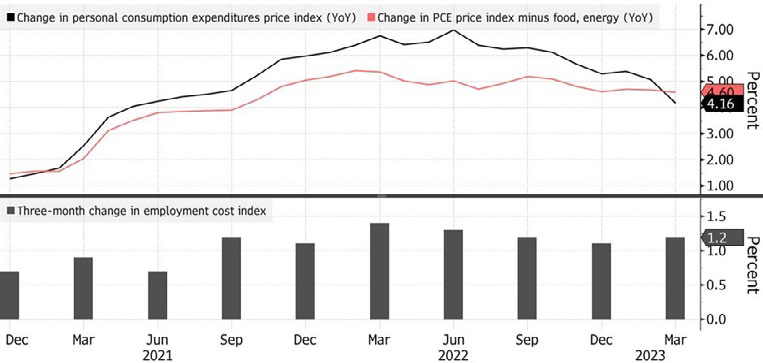

The Fed’s preferred inflation measure, the Personal Consumption Expenditures Price Index, which excludes food and energy prices, rose by 0.3% month-on-month in March and 4.6% compared to the previous year.

Prices still rising at brisk pace inflation remains

elevated, key wage gauge accelerates

So far, interest rate increases haven’t had as significant an impact on growth in developed economies as expected, with the US and European economies skirting a much-anticipated recession until now. The global economy has got off to a better-than-expected start in 2023. Growth in China has significantly exceeded most forecasts, and growth in the US and eurozone has been at least in line with expectations.

A recession later this year is not out of the question, however, with US GDP data coming in below expectations for the first quarter, rising 1.1% versus expectations of a 2% rise.

“DEMAND FOR DIESEL IN THE US CONTRACTED SOME 6% IN THE FIRST QUARTER OF THE YEAR COMPARED WITH THE PREVIOUS YEAR”

Possibility of a recession in the next 12 months

according to economists surveyed by Bloomberg

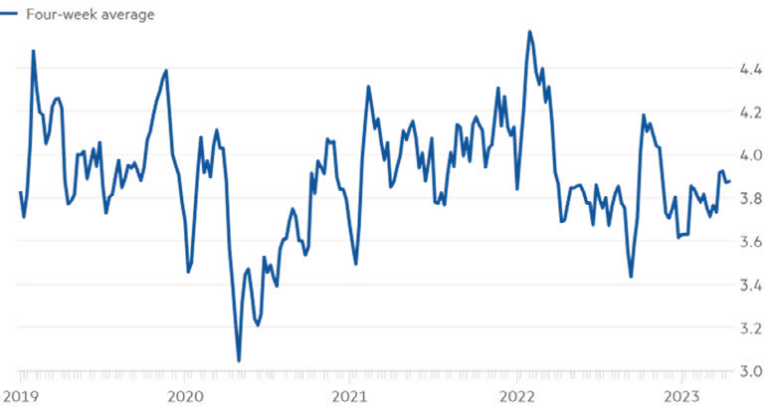

One worrying sign of consumers starting to tighten their belts is the decline in demand for diesel in the US, which contracted some 6% in the first quarter of the year compared with the previous year. Diesel is used in the transportation of goods and this decline reflects a slowdown in trade.

US diesel demand has slumped Distillate fuel oil, million barrels a day

Oil prices have also come off recent peaks, notwithstanding the early-April OPEC announcement that it would be reducing production by 1 million barrels a day in what was already expected to be a year where supply would be tight. Based on mixed economic data from China and US recession concerns, Brent crude oil has declined. almost $10 a barrel to about $75 since early April. China’s manufacturing activity fell in April, the first decline in its Manufacturing Purchasing Managers’ Index since December when it scrapped Covid restrictions.

First Republic brings renewed attention to the banking sector

Of greatest concern in the US is a resurgence in panic about the future of regional banks and broader contagion across the banking sector. The end of the month brought news of the seizure of First Republic Bank by regulators and its sale to JP Morgan. Initially, this was expected to put worries about the US regional banking sector to bed. JP Morgan paid $10.6 billion for First Republic Bank in a deal brokered by the Federal Insurance Deposit Corporation (FDIC) after the bank’s share price collapse. It agreed to take on $92 billion of First Republic’s deposits and to share the losses on some loans. FDIC, in turn, will provide JP Morgan with $50 billion in financing.

Instead of infusing confidence, however, investors responded by offloading regional bank shares, which closed at their lowest levels in three years. The panic sell-off also brought declines in the share prices of larger banks.

Regional bank stocks drop sharply KBW Bank Index

US debt ceiling deadline looms

Adding to investor concerns are US debt ceiling developments that still provide no solution for dealing with the problem by

June, when the Treasury Department risks running out of cash. To date, President Joe Biden has refused to satisfy Republican demands that spending cuts and other cost savings accompany an agreement to increase the borrowing limit.

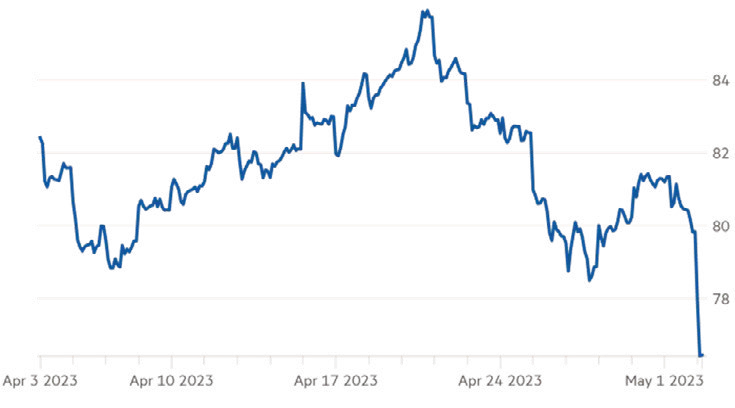

His unbudgeable stance has seen the cost of insuring against a US government default on short-dated debt soar, as evident in the graph below of US credit default swap movements.

US credit default swaps (basis points)

Several scenarios face the US as the so-called X-day – the day the money runs out – approaches. Should Biden hold firm on refusing to negotiate a spending package reduction in return for the Senate agreeing to lift the debt ceiling, the Treasury Department would be forced to delay payments to agencies, contractors, Social Security beneficiaries and Medicare providers. This could require a 20% cut in non-interest federal spending – rising in time to 35% or more – an unsustainable situation for the US government that would effectively leave it unable to function.

The worst-case outcome would be for the Treasury Department to default on its Treasury bill commitments, which would severely undermine the position of the US as a global leader and the US Treasury market as the safest and most liquid market in the world. Yet an outright default is unlikely. Republicans and Democrats will almost certainly be forced into reaching an 11th-hour agreement if they haven’t achieved a resolution before then, given the potentially catastrophic consequences for the country and political damage to the party seen as responsible. However, the ongoing

uncertainty may well bring short-term volatility for the Treasury market.

GLOBAL MARKET RETURNS APRIL 2023

If you would like to hear more detail on the options available to you, get in touch with us today by filling out the form below.

Need assistance with your retirement plans? Talk to Mike today!

Subscribe to the latest news and insights from Imperius Wealth

imperiuswealth.com needs the contact information you provide to us to contact you about our products and services. You may unsubscribe from these communications at anytime. For information on how to unsubscribe, as well as our privacy practices and commitment to protecting your privacy, check out our Privacy Policy.