COMMODITIES, BONDS AND EQUITIES LOWER DESPITE TECH ADVANCES

It was a month when this year’s acute focus on US Fed interest rate moves shifted to the possibility of a US government debt default as the debt ceiling threatened to be breached in early June. As expected, at the 11th hour, House speaker Kevin McCarthy and President Joe Biden reached agreement – one that is broadly viewed as not satisfying either party’s desires.

Against this backdrop and ongoing inflationary pressures, stock markets had a muted to negative month, with only the tech sector performing well. The Nasdaq advanced 7.7% during May, well ahead of the S&P 500’s 0.4% increase. European and UK stock markets retreated by 2.0% and 4.7% respectively. China’s CSI300 also fell into negative territory following disappointment about the longevity of the economic rebound in the wake of December’s lifting of Covid restrictions. The Bloomberg Commodity Index ended 5.6% lower.

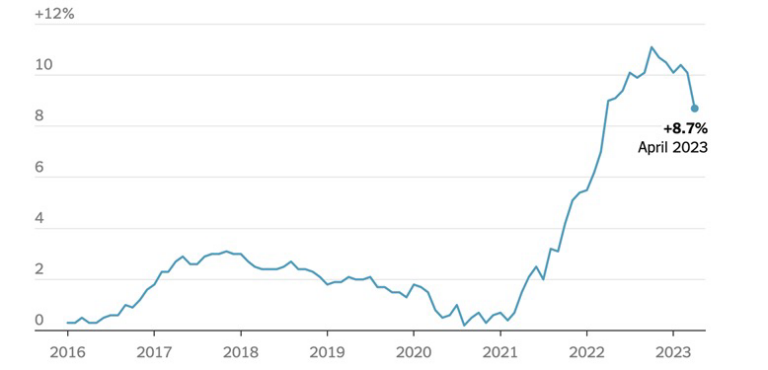

Inflation starting to ease but particularly sticky in the UK

The month’s most disappointing economic news was on the inflation front, which is proving far stickier than expected. Food price inflation remains in double-digit figures across the world, giving further credence to views that there may be “greedflation” at play in the industry. In contrast, China price increases are verging on deflationary because of an economy that is experiencing completely different drivers to those present in western developed economies.

In the UK, a core inflation rate of 6.2% in April was the highest rate since February 1992, while the headline index was 8.7% versus 10.1% the previous month. Latest retail price inflation figures released by the British Retail Consortium came as a shock, recording a 9% increase versus 8.8% in April – the highest levels since the index was introduced in 2005. Food price inflation remained above 15%, at 15.4% versus the previous month’s 15.7%.

"STOCK MARKETS HAD A MUTED TO NEGATIVE MONTH, WITH ONLY THE TECH SECTOR PERFORMING WELL"

Annual change in Britain’s Consumer Price Index

The Fed’s preferred inflation measure, the Personal Consumption Expenditures Price Index, which excludes food and energy prices, rose by 0.3% month-on-month in March and 4.6% compared to the previous year.

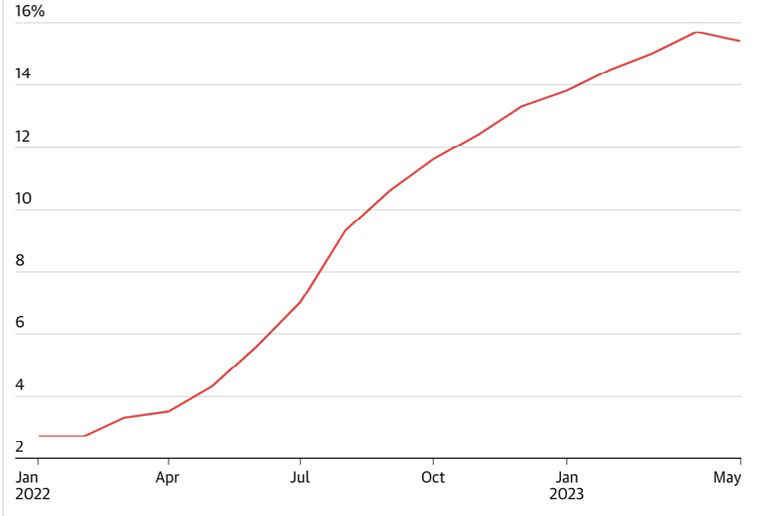

UK food inflation eased to 15.4% in May Annual food-price inflation

In Europe, agricultural and energy prices are falling but food prices remain high. Flash inflation figures for Spain did fall more than expected in May and there is optimism for similar positive news elsewhere in Europe.

Meanwhile, in the US, the Federal Reserve’s preferred inflation measure, the core Personal Consumption Expenditures Price Index, increased 0.4% between March and April, ahead of the anticipated 0.3%. Consumer spending remains robust, rising

0.8% in April, also coming in well ahead of the consensus forecast of 0.4%.

Inflation rate trends in emerging markets are looking more encouraging. In Brazil, the April inflation rate was 4.2% compared with 4.7% and the lowest rate since October 2020. Despite pressure on the central bank to reduce interest rates, it is likely to want to see core inflation coming down meaningfully and inflation expectations declining before reducing interest rates.

China’s inflation rate came in at 0.7% in April, its weakest rate since February 2021. Focus Economics attributes the weak overall price pressures in China in recent months to improved supply chains, soft commodity prices and domestic demand still not firing on all cylinders.

Given the persistence of food price inflationary pressures, central banks are expected to keep a tight rein on monetary policy. Traders are pricing in another rate hike in the US at the Fed’s upcoming meeting on June 14 and possibly another one thereafter. Swap contracts have increased to 5.37%, more than 25 basis points above the current effective fed funds rate.

“IN THE UK, A CORE INFLATION RATE OF 6.2% IN APRIL WAS THE HIGHEST SINCE FEBRUARY 1992”

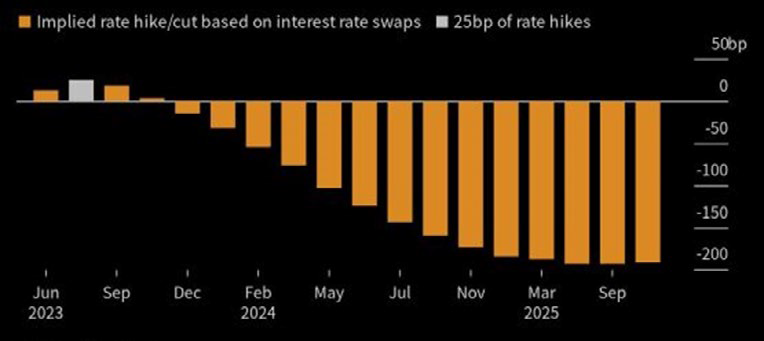

What’s priced in?

Swaps price in 25bp of rate hike premium priced by July Fed policy meeting

Recession risks remain

The sharp fall in energy prices and better than expected data on economic growth has meant that in Europe and the UK, where recession was seen as a near certainty just a few months ago, there is now the potential for it to be averted. Consumers are still able to draw on savings built up during the pandemic.

In the US, these savings have been depleted and a recession may be seen as acceptable to the Fed to reduce wage inflation from 5% to the 3% level commensurate with their 2% inflation target. However, with gains in food prices, energy prices, housing costs and used car prices all slowing – and money supply dropping off a cliff – policymakers face a significant balancing act.

Gross domestic product data, the traditional measure of economic activity used to assess whether an economy is in recession, remains positive but real gross domestic income declined in the first quarter this year and US corporate profits fell by 5.1%. There is always a lag in the impact of rate increases. Despite some of the most recent data suggesting risks of a recession have diminished in the short term, they very much remain for late 2023 moving into 2024.

Tech shares provide resilience with enthusiasm for AI applications soaring

Tech stocks have dominated the US stock market this year, with Meta and Nvidia rising more than 100% and Nvidia becoming a $1 trillion company in the last week of May on the bullish outlook for artificial intelligence and its likely dominance in this new economy trend.

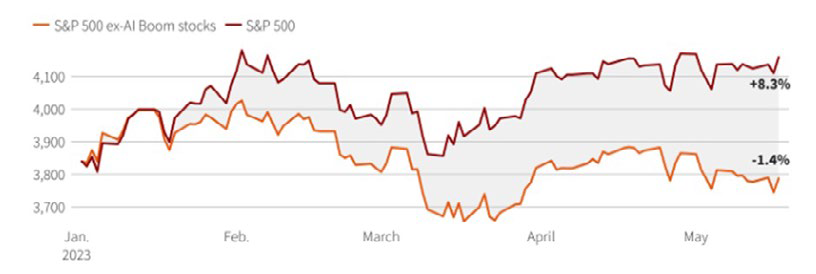

AI stocks boosting US stock market

Removing a group of artificial intelligence-linked stocks from the S&P 500

would have cut the index’s performance by about 10 percentage points this

year, according to Societe Generale analysis

The ‘Big Six’ (Apple, Microsoft, Google parent Alphabet, Amazon, Nvidia and Facebook owner Meta Platforms) tech stocks now have a combined valuation of about $10 trillion and make up more than 25% of the S&P500’s market capitalisation. The AI rally has driven the Nasdaq Index more than 24% higher this year.

Interest in the stocks was propelled by the US regional banking crisis in March, when investors thought that the Fed would be pressured into easing off on interest rate hikes to avoid a systemic financial crisis. Arguably, these shares have become ‘virtual’ utilities, with greater defensive qualities than a year ago thanks to their ability to ride out this year’s economic uncertainties. The outlook looks bright for them if AI takes off as expected because they all have ambitions, and propositions, to capitalise on demand for AI-enabled products.

The dominance of the Big Six is, however, seen by some investors as a cause for concern as the US stock market’s fortunes have largely been dependent on the performance of this narrow group of stocks. This could mean more volatility ahead if the US does fall into recession. Stubbornly high inflation, the impact of interest rate increases already put in place, and the possibility of more could dent the outlook for these behemoths. It’s the first time since the 1960s that a handful of stocks have dominated the broader stock market so significantly and this time it is companies in the same sector, with valuations determined by the same macro and micro economic dynamics.

GLOBAL MARKET RETURNS APRIL 2023

If you would like to hear more detail on the options available to you, get in touch with us today by filling out the form below.

Need assistance with your retirement plans? Talk to Mike today!

Subscribe to the latest news and insights from Imperius Wealth

imperiuswealth.com needs the contact information you provide to us to contact you about our products and services. You may unsubscribe from these communications at anytime. For information on how to unsubscribe, as well as our privacy practices and commitment to protecting your privacy, check out our Privacy Policy.