JULY SEES EQUITY MARKETS RALLY FURTHER, BONDS

RETREAT AGAIN AND COMMODITIES RECOVER

Equity investors in developed markets were emboldened by continued economic resilience in the face of sky-high interest rates and inflation entering disinflation territory. Meanwhile, bonds weakened further as central banks continued to hike rates, putting paid to expectations that 2023 may be the Year of the Bond.

Markets now anticipate that the peak rate is near in the US but that there may be further hikes in Europe.

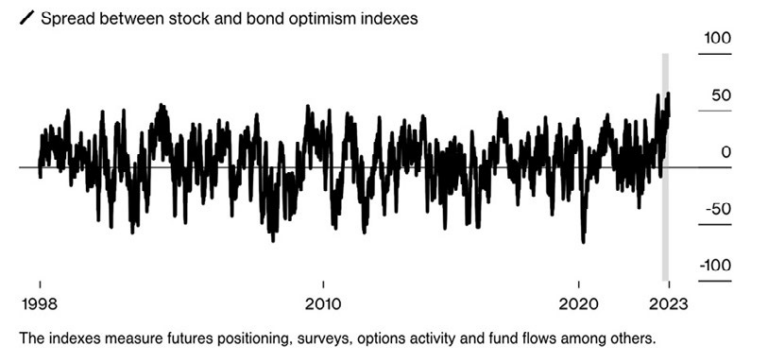

Record stocks versus bonds optimism

Sentiment about equities against bonds is the highest it has been in 24 years

Optimism in equities over bonds bolstered the FTSE World TR index by 2.3% in July. Japan’s Nikkei was the only major equity market to show a small decline. China’s CSI 300 gained almost 4% for the month, dragging the index out of negative territory for the year and leaving it 3.1% higher year to date.

After a weak first half, commodities surged across the board during July. Oil led the gains with WTI Crude up 15.8%. This came after production cuts by OPEC+, and in particular by Saudi Arabia, the world’s largest exporter. Gold was up by 2.4% and silver by 8.7%.

"BONDS

WEAKENED

FURTHER AS

CENTRAL BANKS

CONTINUED TO

HIKE RATES"

Has positive equity sentiment gone too far with economic data still mixed?

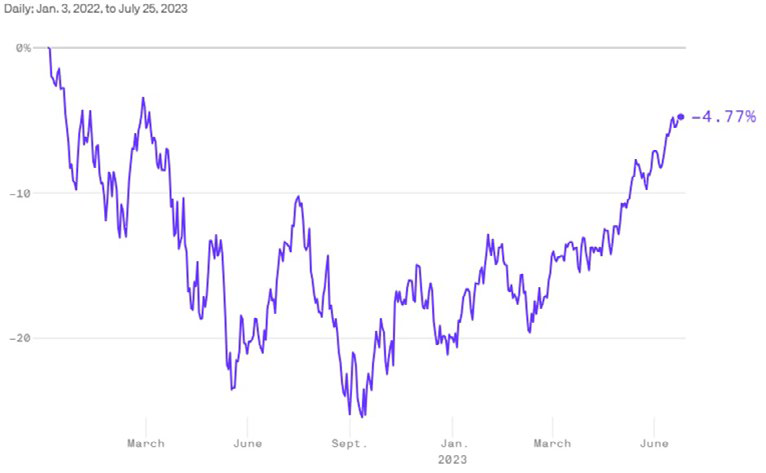

There are some concerns about whether there is too much optimism being priced into stock markets currently. The S&P500 is within 5% of its 2020 high even though there are still significant macro-economic and geopolitical uncertainties ahead. The big tech favourites, described as the Magnificent Seven and comprising Nvidia, Meta, Tesla, Microsoft, Apple, Amazon, and Alphabet, continue to drive the upward rally in US stock markets. During the month, the Nasdaq’s 3.8% still outpaced the broader based S&P500’s 3.2% but by a smaller margin than in previous months.

Change in S&P 500 since all-time high

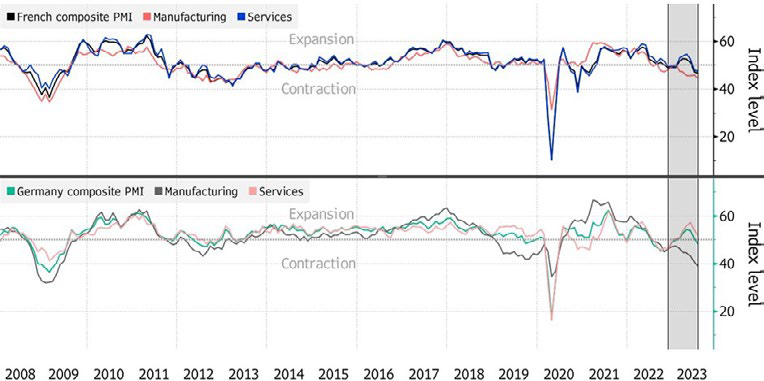

Hopes of an end to the manufacturing recession were dashed by the release of flash July purchasing managers’ indices in the developed markets, which showed that manufacturing remained in contractionary territory.

The US was the only developed market to beat expectations, coming in at 49 versus 46.2. Germany and France’s manufacturing PMIs looked particularly disappointing, coming in well below expectations. France suffered its 11th consecutive contraction in the index.

There is also emerging evidence of the service sector beginning to slow down. The Services Index declined for the first time in six months, with PMIs across the developed world, including the US, coming in lower than expected by the market and getting closer to 50 – the dividing line between expansionary and contractionary territory. France’s PMI fell further into contractionary territory, coming in at 47.4 compared with economists’ expectations of 48.4.

“CHINA’S CSI

300 GAINED

ALMOST 4% FOR

THE MONTH,

DRAGGING THE

INDEX OUT

OF NEGATIVE

TERRITORY FOR

THE YEAR”

German and French economies are nosediving

Hope for Goldilocks scenario in US

Notwithstanding the disappointing PMIs, expectations are shifting to the belief that the US Federal Reserve will be able to navigate its much-debated soft landing, bringing the world’s economy into Goldilocks territory, with economic conditions not too hot or too cold but just right. The hope is the economy will withstand fallout from the 11 rate hikes that have been implemented by the Fed, taking the target range for the federal funds rate from 5.25% to 5.5% in July.

At the July meeting, Fed Chair Jerome Powell told journalists: “We’ve seen so far the beginnings of disinflation without any real costs in the labour market. That’s a really good thing.”

According to the National Association for Business Economics’ (NABE) July survey, 71% of forecasters believe a recession is unlikely in the coming year compared with 42% in January. The NABE Survey Panel foresees the US economy experiencing rising sales and improving profits, with lower material costs and stabilising wages.

Contributing to the better sentiment was second-quarter gross domestic product data, which came in higher than expected at 2.4%, supporting the case for a soft landing. The Fed’s preferred measure of inflation, excluding food and energy, was lower than expected at 3.8% annualised, signalling disinflation as the measure gets closer to the central bank’s 2% target.

Need assistance with your retirement plans? Talk to Mike today!

Subscribe to the latest news and insights from Imperius Wealth

imperiuswealth.com needs the contact information you provide to us to contact you about our products and services. You may unsubscribe from these communications at anytime. For information on how to unsubscribe, as well as our privacy practices and commitment to protecting your privacy, check out our Privacy Policy.