POSITIVE START TO 2023 FOR EQUITIES

Developed world stock markets started the year positively but performance became more muted after widespread gains in January. The recent collapse of Silicon Valley Bank and the rescue of Credit Suisse bank by UBS unnerved investors while central banks restated their intentions to continue increasing interest rates to combat inflation.

Renewed interest in the tech sector saw the Nasdaq surge 20.8%. In contrast, the Dow Jones Industrial Average only just inched back into positive territory at the end of March amid concerns of contagion from the banking crisis.

Shares in most European markets also rallied during the quarter on improving economic fortunes as the eurozone overcame its

dependence on Russian gas during a much milder winter than usual. However, the demise of Credit Suisse dampened investor confidence and in the UK, where banking is a particularly important market sector, the FTSE All-Share index declined 2.8% in March to end the quarter up 3.1%.

Emerging markets and in particular Chinese equities do not yet seem to have factored in the improving economic fortunes of the world’s second-largest economy. The SSE Composite gained 5.9% during the first quarter but retreated during March. Yeah Meanwhile, the SSE India Index is 7.0% lower this year.

Bond markets exhibited extreme volatility throughout the entire period. Short-dated treasury yields dropped at the fastest rate since 1987 as awareness of the banking crisis emerged. Much of the fall was then reversed and most bond markets ended the quarter broadly unchanged.

Except for gold, commodities had a poor start to the year and the oil price declined each month.

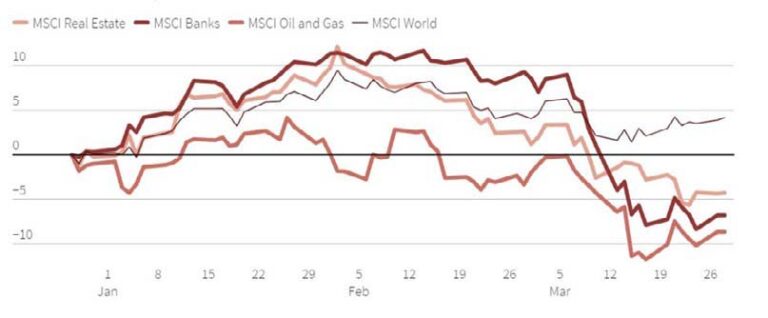

At a global level, despite positive performance for many sectors, economically sensitive sectors remain underwater, with banks experiencing their worst month in three years.

"SHORT-DATED TREASURY YIELDS DROPPED AT THE FASTEST RATE SINCE 1987 AS AWARENESS OF THE BANKING CRISIS EMERGED"

Economically sensitive sectors falter

Banks set for worst month in three years Concerns about the industry hit banking shares

World economy in a lost decade?

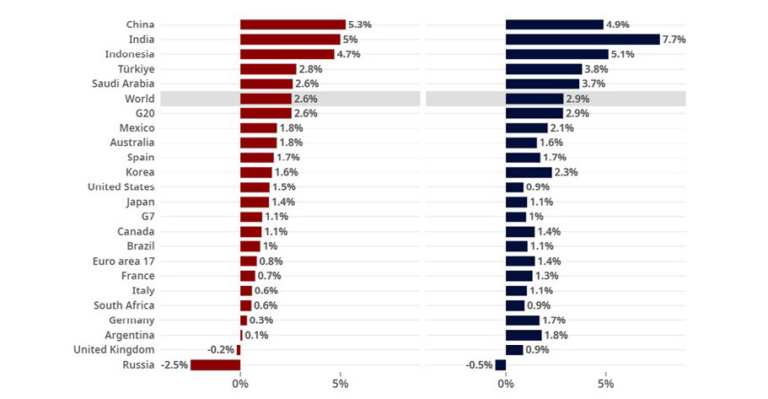

On the economic front, the OECD expects growth to remain at below-trend rates in 2023 and 2024, with its projected global growth for this year at 2.6%. Meanwhile, the World Bank has warned that we are heading for a lost decade for the world economy.

It argues that nearly all the economic forces that powered progress and prosperity over the last three decades are fading. It predicts average global GDP growth will reduce by about a third to 2.2% between 2022 and 2030 and warns that declines would be even steeper in the event of a global financial crisis or a recession.

Real GDP growth projections for 2023 and 2024

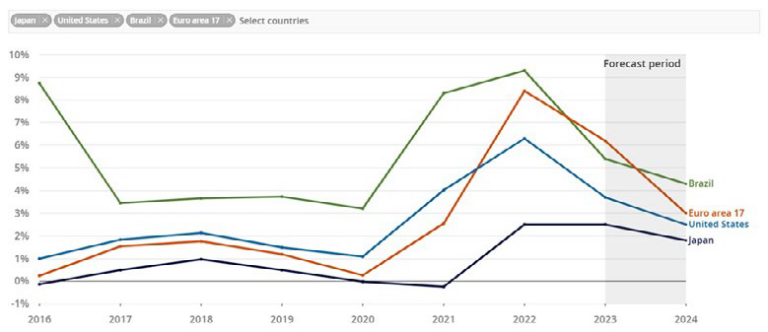

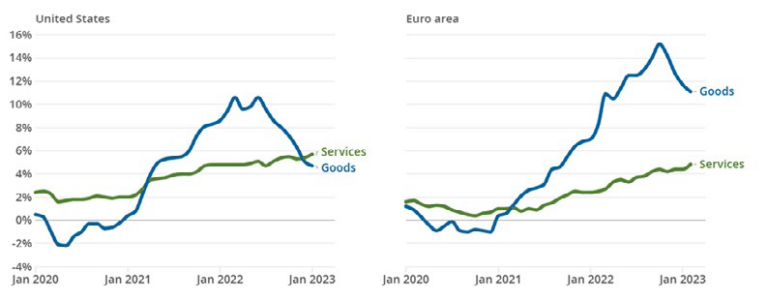

The OECD also anticipates that headline inflation across the G20 countries, which has begun falling mainly due to an easing of energy and food prices, will continue to ease. However, it notes that services inflation remains on an upward trajectory in both the US and eurozone.

Headline inflation

Services inflation is still rising

“A SURPRISINGLY STRONG LABOUR MARKET CONTINUES TO BE THE FINAL DOMINO THAT NEEDS TO FALL BEFORE THE FED CONSIDERS REDUCING THE FED FUNDS RATE AGAIN”

Heading off a banking crisis

The failure of two regional banks, Silicon Valley Bank and Signature Bank, and the takeover of Credit Suisse in mid-March introduced significant financial market volatility and fears of contagion spreading further afield. It also raised concerns that these problems, largely due to unseen liabilities in the smaller banks, may be more widespread and could be a precursor for another global financial crisis.

Consequently, the US Central Bank stepped in to guarantee the deposits of the two banks that went into bankruptcy and engaged in coordinated measures to ensure there was sufficient dollar liquidity in Europe in the wake of Credit Suisse’s demise to limit the

effect on other banks in the eurozone.

Market participants interpreted these measures as being likely to result in a more restrained approach to interest rate policy.

Markets’ rate expectations have radically shifted since banking turmoil began Shift in expectations of level of key interest rates six policy meetings from now

However, the Fed and eurozone quickly put paid to those expectations when they raised rates during March and stated they were still committed to aggressively fighting inflation. In the US, a surprisingly strong labour market continues to be the final domino that needs to fall before the Fed considers reducing the Fed Funds Rate again.

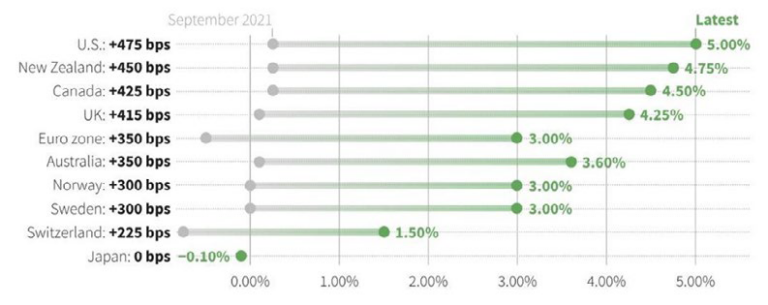

The race to raise rates Change in policy rates by central banks overseeing the 10 most traded currencies since the start of the interest rate tightening cycle in September 2021

“FED CHAIR JEROME POWELL HAS ALSO ACKNOWLEDGED THAT THE BANKING CRISIS COULD HAVE THE “EQUIVALENT” IMPACT OF AT LEAST ONE QUARTER-POINT RATE INCREASE”

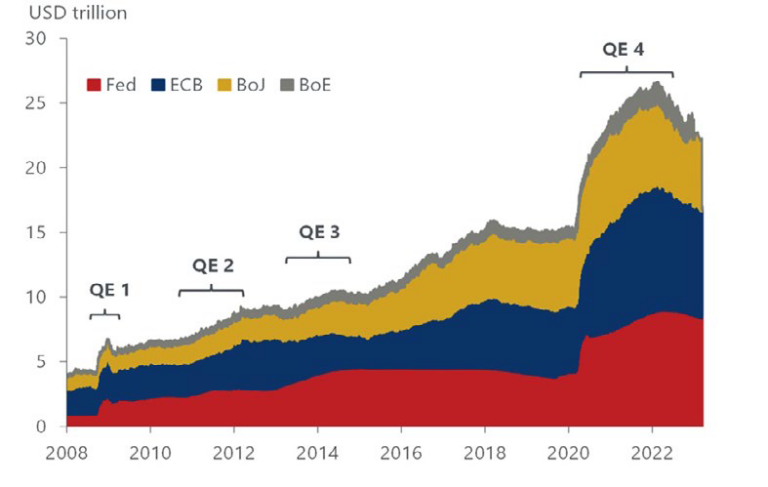

In addition to raising rates, the Fed has committed to withdrawing $95 billion monthly from the financial markets until it has sufficiently wound down its balance sheet. Société estimates that a $2 trillion reduction in the Fed’s balance sheet would equate to an almost 2.5 percentage point increase in the Fed Funds Rate. Fed chair Jerome Powell has also acknowledged that the banking crisis could have the “equivalent” impact of at least one quarter-point rate increase.

AE central bank balance sheets are still vastly inflated Central bank total assets

Sustainability surges

Businesses are again prioritising their environmental impact as the reality of the long-term risks of climate change become real.

According to the World Economic Forum, the transformation in attitude has been catalysed by growing customer awareness,

more robust regulation and increasing demands in this area from investors and banks. It notes that more companies have set net-zero goals, investments in sustainability issues have exploded, and new departments and roles have been created whose purpose

is to tackle an ESG agenda.

In Europe, decarbonisation initiatives have been fast-tracked, with EU carbon credits reaching record highs of more than €100 a tonne, as companies seek to avoid the higher cost of carbon allowances and the corresponding impact on their profitability. Regulations in the EU oblige companies operating in gas, coal power generation or industrial manufacturing to buy carbon credits, with one credit allowing the company to emit one tonne of carbon.

European carbon reaches €100 a tonne

Investment strategy during the quarter

To reflect the growing recognition of the importance of the EU carbon allowance market and its seasonality, additional tactical exposure was added to the strategy at the start of the year ahead of the April deadline for companies to secure the allowances they need to surrender (which in the past has resulted in significant last-minute buying). Furthermore, the annual announcement due in May of the total number of allowances in circulation has historically resulted in a rally as companies digest how tight supply will become.

Earnings revisions and relative valuation suggest there is still further to go in the recovery of shares with value characteristics.

US high dividend exposure was added to the strategies in January. This was negatively affected by the banking crisis but these types of company are now well-placed even in the event of a challenging economic environment.

Some of the exposure to India was switched to China with Indian equity valuation metrics starting to drop from elevated levels (but

still the highest of major markets). The opening up of China following its latest Covid lockdowns has progressed quicker than

expected and a pivot in government policy – which has softened regulation and increased market support – has been seen as a boost for GDP growth, leading to a decline in risk.

With inflation expectations subsiding, some inflation linking has been removed from bond exposure. European transport exposure was also reduced to capitalise on a short-term rally and reduce risk from the impact of an increasingly hawkish European Central Bank.

After the market rally in January, cash levels in the strategy were increased but partially redeployed at the end of the quarter to capture the rebound of smaller companies that had declined during the March sell-off. Fund exposure was added to the UK FTSE 250 and to global thematic technology, including companies involved in the sustainable future of food supply. Balances of Japanese yen and Swiss franc have been retained and continue to provide a haven during periods of weak market sentiment.

If you would like to hear more detail on the options available to you, get in touch with us today by filling out the form below.

Need assistance with your retirement plans? Talk to Mike today!

Subscribe to the latest news and insights from Imperius Wealth

imperiuswealth.com needs the contact information you provide to us to contact you about our products and services. You may unsubscribe from these communications at anytime. For information on how to unsubscribe, as well as our privacy practices and commitment to protecting your privacy, check out our Privacy Policy.