Is your pension costing you more than €450,000 over a 10 year period and you don't know it?

Is Your Pension Costing You €450,000 Over 10 Years?

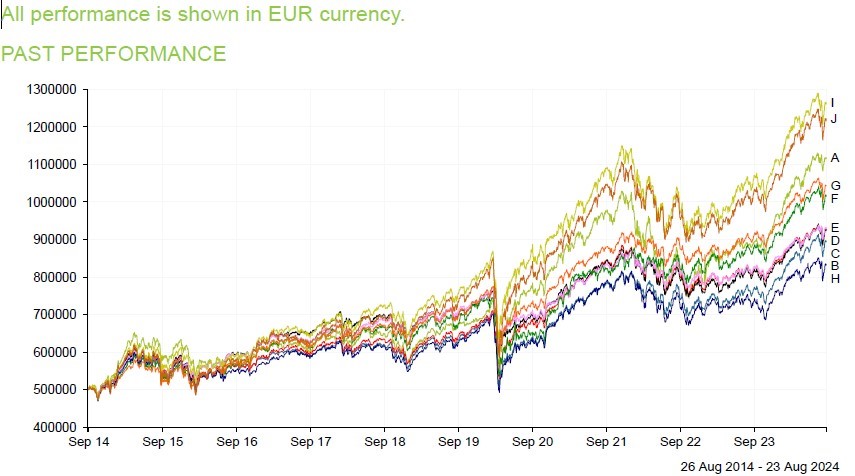

Pension Fund Performance – since 26/08/2014 to 26/08/2024

– Irish Pension Fund Managers

Strong results generally but material variance between ‘Best ‘and ‘Worst’ in class.

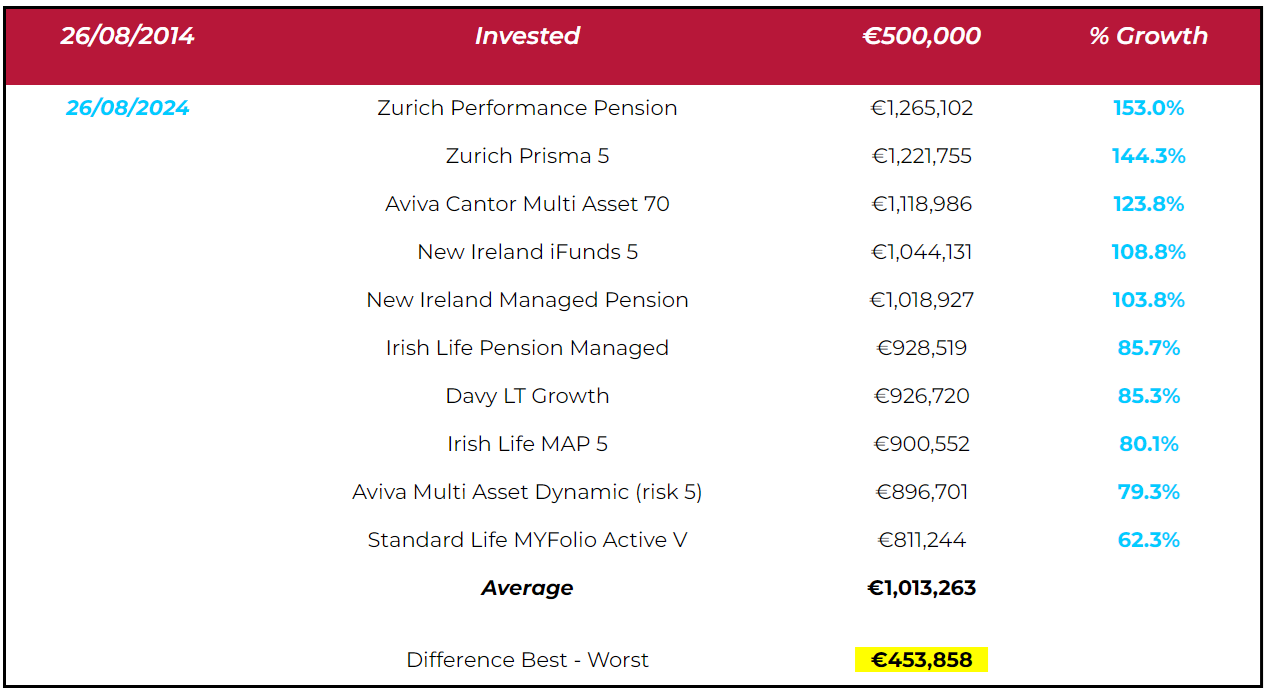

How has a €500,000 Pension fund invested for 10 Years since 26/08/2014 to 26/08/2024 in ten similar rated funds performed with the respective Pension Managers?

| 26/08/2014 | Invested | €500,000 | % Growth |

|---|---|---|---|

|

26/08/2024 |

Zurich Performance Pension

|

€1,265,102 |

153.0% |

|

|

Zurich Prisma 5 |

€1,221,755 |

144.3% |

|

|

Aviva Cantor Multi Asset 70 |

€1,118,986 |

123.8% |

|

|

New Ireland iFunds 5 |

€1,044,131 |

108.8% |

|

|

New Ireland Managed Pension |

€1,018,927 |

103.8% |

|

|

Irish Life Pension Managed |

€928,519 |

85.7% |

|

|

Davy LT Growth |

€926,720 |

85.3% |

|

|

Irish Life MAP 5 |

€900,552 |

80.1% |

|

|

Aviva Multi Asset Dynamic (risk 5) |

€896,701 |

79.3% |

|

|

Standard Life MYFolio Active V |

€811,244 |

62.3% |

|

|

Average |

€1,013,263 |

|

|

|

|

|

|

|

|

Difference Best – Worst |

€453,858 |

|

Comments

- The graph and the table above demonstrate the cumulative returns achieved by the individual Pension fund managers over the 10-year period.

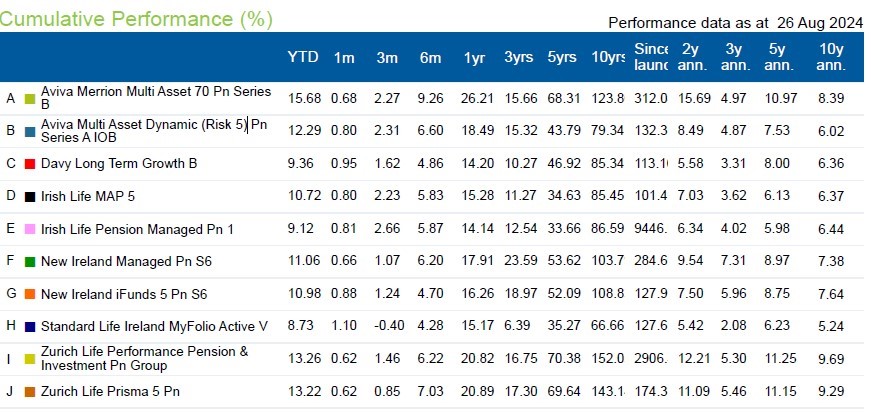

- Over a 10-year investment period, the annualized returns for these multi-asset fund strategies {Equities/ Bonds/ Commodities/Cash & Alternatives} have ranged from 69% (Best) to 5.24% (Worst).

- Looking under the bonnet on these various funds’ performance, shows that a €500,000 pension invested on 26/08/14 in the best performing fund would have grown by c. 153% to a €1,265,102 cumulatively (gross of an annual management charge) while the worst performing fund grew 3% to c. €811,244 (gross of an annual management charge).

- Accumulated that is a difference of over €453,000, a very material amount which should prompt a Pension Investor to request a detailed performance review and critique of his managers fund performance.

- At Imperius Wealth, we are not happy to set the bar at average fund performance and we regularly review our client’s funds’ performance against similarly risk rated Irish based funds. Meeting with our clients (semi-/annual reviews) means that we identify underperforming funds and can recommend corrective action (including fund switches & reduced charges). We encourage a ‘hands- on’ approach with our clients, with regular market updates and valuations.

- Taking a hands-off approach to your Pension funds risks falling into the ‘Average’ or ‘Underperforming’ bucket and can result in delaying your retirement plans by several years.

Data Source

- The data inputs for this comparative fund review are available to retail intermediaries and are collated and reported monthly by the independent consultant Rubicon Investment Consulting

- All funds reviewed had performance data for a full 10-year comparison.

- The funds shown have a similar risk rating {ESMA 5 equivalent}

What Can I Learn From This?

- A Pension Investor should not be concerned about short term performance (< 1 year) but should critically review their pension manager performance over a longer 3–5-year period.

- He/she should request from their financial adviser comparative data on how other managers in similar risk rated funds performed over the same time.

- If your Pension Manager has achieved average returns or worse, then an investor should strongly consider moving his fund to a manager with a better track-record.

- A Pension Investor should schedule a pension review meeting with an experienced Financial Adviser to guide through the many fund options to pick an appropriate fund for their risk appetite, review the various charges and the managers performance record. Fund charges vary but typically are in a range of 0.75% – 1.25% p.a., but it is pension fund performance over a 3-5 year period that is a key guide.

- Just like a commitment to regularly hit the gym to improve your health, to improve your pension fund performance requires an action plan and a pro-active Investor approach to review and make fund/ manager changes when the research stacks up.

- Don’t be lethargic, take control of your Pension Assets, which may be your largest single asset after your home. A commitment to regular annual pension review meetings with an experienced qualified financial adviser, can with time result in the difference between achieving ‘Average returns’ and ‘Best in class

Summary

If you think your Pension fund performance has been ‘Average’ or worse, then its time to give it a fitness check. Average or below performance should not be acceptable, take a hands on approach and request your latest annual pension statement, and arrange a meeting with one of our qualified financial planners, E-mail us: hello@imperiuswealth.com or fill out the form below, where we will assess your pension funds performance to make sure that it is well positioned for the next 1-3 years.

Subscribe to our quarterly newsletter.

By submitting this form, you agree to receive emails from Imperius Wealth. You may unsubscribe from these communications at any time. For information on how to unsubscribe, as well as our privacy practices and commitment to protecting your privacy, please review our Privacy Policy.