Irish Savers Should Move Cash as AIB and Bank of Ireland Sit Tight

Irish Savers Should Move Cash as AIB and Bank of Ireland Sit Tight

It feels like the entire country went to bed one night in early August and set the alarm clock for 2008. The country’s banks found themselves back as public enemy number one. Like Scooby Doo villains, they are “up to their old tricks” and “cheating people”. A decade of rehabilitation vanished.

The pillorying centred on the failure to pass on increases in European Central Bank (ECB) interest rates to depositors, while inflicting higher rates on mortgage holders, largely those on trackers.

Worse of all, the banks are making enormous profits, and are poised to funnel large cash returns to shareholders. Bank of Ireland, which last week was at the centre of yet another Irish banking IT screw-up, is also rewarding its executives with share options. It’s a damning narrative.

A survey by rating agency S&P found that Irish banks were the most parsimonious in Europe when it comes to rewarding depositors in the current interest rate cycle. Between June 2022 and May 2023, British banks passed on 43 per cent of rate rises to savers, compared to just 7 per cent here.

The euro area average pass through was 20 per cent. When Italian bankers passed “only” 11 per cent of recent rate rises to savers, it prompted the government to levy a windfall tax.

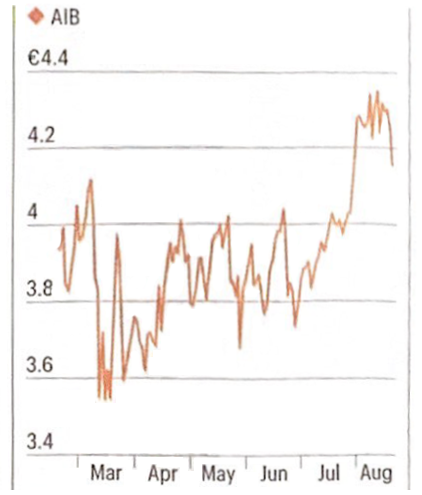

The banks here say that they have taken a more “balanced” approach to rate rises. ECB rates have jumped by 425 basis points (bps) since July 2022. Yet AIB, for example, has only passed on 50 bps to its variable-rate mongage customers, excluding tracker holders ’ where it is contractually obliged to pass all hikes. Since last May, rates for new mortgages here went from near worst of the eurozone to near best, before settling around the average. Favouring borrowers over savers is not a balanced approach. For the banks, it makes a lot of sense.

For a start, Irish banks have too much deposits and not enough loans. At the end of 2022, AIB loans to deposits ratio was 58 per cent, compared to 95 per cent at Lloyds. Increasing rates would attract savings from the post office, credit unions or other banks.

A greater disincentive can be found with the deposit profile of the banks. AIB has €102 billion of deposits; of that €64.4 billion is in current accounts, and attracts no interest. A further €32.6 billion is demand deposits which attract very low interest. The bank has only €5.3 billion of term deposits, or what we normally consider to be savings.

A decade ago, 60 per cent of the bank’s deposits were term.

Up to last year, current accounts and demand deposits were a loss-making activity for the banks. From 2014 to 2022, the ECB charged the banks negative interest for holding this so-called overnight money. Since the rates shifted, the banks now deposit this cash at the European Central Bank, where it earns

3.75 per cent. As KBC and Ulster Bank exited the market, customers were forced to switch to the big three of AIB, Bank of Ireland and Permanent TSB, further boosting the current account balances. On top of that, household savings mushroomed during the pandemic. As a result, the current account is now the golden goose. AlB’s net interest income will be over €3 billion this year, or 50 per cent above the levels it earned before the ECB rate-tightening began. Irish banks have gone from the least to most profitable banks as measured by net interest margin.

So there is no clear incentive for the banks to divert cash from overnight money to term deposit by raising the rate on savings. It’s quite the opposite.

Ironically banks actually charge people a fee to maintain a current account, while making massive profits out of the money lying so idly within them. By keeping new lending rates low, on the other hand, the pillar banks have successfully driven non-bank lenders out, of the mortgage market.

S&P noted that the banks slowest to pass on rate rises to depositors were those worst hit in the eurozone crisis: in Spain, Italy, Greece and Ireland. These are the markets where there has been the most consolidation.

With little domestic competition, the banks here exert unfettered control on rates.

Rather than waiting for government or Central Bank intervention, depositors could move their money. Raisin.ie, a German online deposit broker, can get savers a rate of 4 per cent with, ironically, ltalian bank BFF, guaranteed up to €100,000. This compared to 1.25 – 1.5 per cent with Irish banks.

Expect no big shift from the Irish banks. After all, their profits will be most sensitive to rate decreases. Hay will be made while the rate rise sun shines. brian.carey@sunday-times.ie

Our Thoughts

- Irish Banks are very well capitalized, are making extraordinary profits and are not passing on ECB interest rate increases to their Depositors.

- ECB rates have increased by 4.25% since 07/2022 yet Irish Bank Deposit rates languish at a measly 1.25-1.50%, the lowest in the EU.

- A recent S&P survey outlined that Irish banks are the least generous in rewarding Depositors, for example UK Banks passed on 43% of their interest rate rises versus a figure of 7% by Irish Banks. The EU average was 20%.

- As Irish Banks have surplus Deposits, in reality they dont need to pay up for Deposits and this is unlikely to change anytime soon. With only three main Irish Banks there is little domestic competition for Deposits.

- Irish Depositors should make their surplus funds earn better returns by investing in higher rated EU Banks that pay 3.50-3.75% deposit rates for 2-3 year terms.

- Imperius Wealth as a broker can show our clients the following attractive headline deposit rates from highly rated Banks.

| Institution | S&P Rating | Term | Indicative Return |

|---|---|---|---|

|

Barclays Bank PLC * |

A+ / Stable |

3 Years |

3.50% |

|

Societe Generale ** |

A / Stable |

3 Years |

3.74% |

Are you looking for sound financial advice? Get the ball rolling with an initial consultation to finally get your finances in order. Get in touch with Imperius Wealth today to make smarter, better-informed decisions.

Email Andrew Cree at andrew.cree@

Need assistance with your retirement plans? Talk to Andrew Today!

Subscribe to our quarterly newsletter.

By submitting this form, you agree to receive emails from Imperius Wealth. You may unsubscribe from these communications at any time. For information on how to unsubscribe, as well as our privacy practices and commitment to protecting your privacy, please review our Privacy Policy.