If you're over 40, you should take a ‘Hands-on Approach’ to your Annual Pension Statement.

If your over 40, you should take a ‘Hands-on Approach’ to your Annual Pension Statement.

If you're over 40, you should take a ‘Hands-on Approach’

to your Annual Pension Statement.

Did you know? 43% of 35-54-year olds expect financial hardship in retirement, and over 50% of the population is expected to have some level of debt when they reach retirement age.

Source: https://www.aviva.ie/pensions/aviva-pensions/retirement-bond/

- Whilst any younger readers (< 40yrs) can be excused for taking a passing interest to their annual Pension statement, those over 40+ should take a greater ‘hands-on approach’ to managing and reviewing their annual Pension statement.

- While most people I speak to fully understand the tax benefits of a regular /annual contribution to their pension, many struggle to get a picture on what their retirement income might look like, the income they need to sustain their lifestyle at a normal retirement age (65 or 66 yrs) and the regular income they can expect on reaching this retirement age.

- The Irish Pension system is fair and supportive of pension saving, most couples/ individuals in Ireland will pay a significantly lower tax rate on their retirement Income, for example at retirement age a married couple can earn up to €36,000 annually @ Nil tax rate.

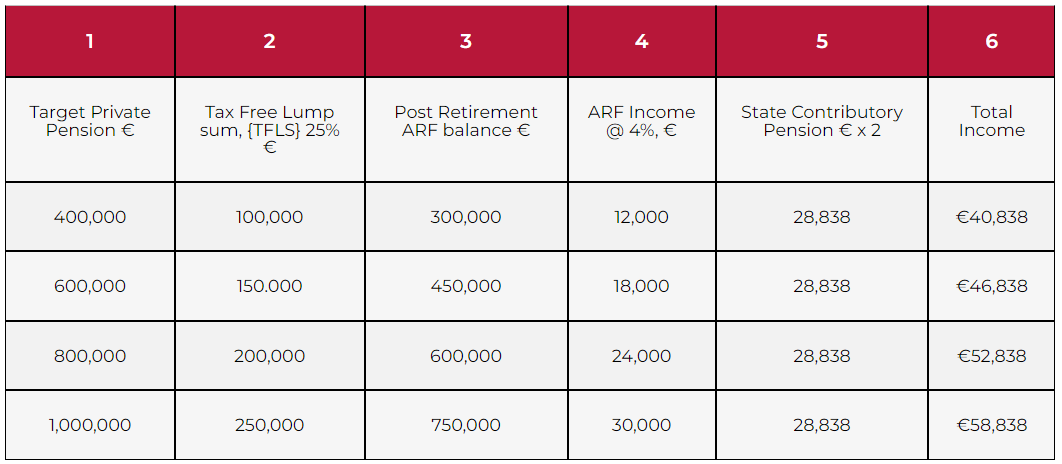

What total Income can I / We expect at a Retirement age of 66 years?

Married Couple (incl. the State Contributory Pension)

| 1 | 2 | 3 | 4 | 5 | 6 |

|---|---|---|---|---|---|

|

Target Private Pension € |

Tax Free Lump sum, {TFLS} 25%

€

|

Post Retirement ARF balance € |

ARF Income @ 4%, € |

State Contributory Pension € x 2 |

Total Income |

|

400,000 |

100,000 |

300,000 |

12,000 |

28,838 |

€40,838 |

|

600,000 |

150.000 |

450,000 |

18,000 |

28,838 |

€46,838 |

|

800,000 |

200,000 |

600,000 |

24,000 |

28,838 |

€52,838 |

|

1,000,000 |

250,000 |

750,000 |

30,000 |

28,838 |

€58,838 |

https://www.gov.ie/en/publication/927721-state-pension-contributory-rates/

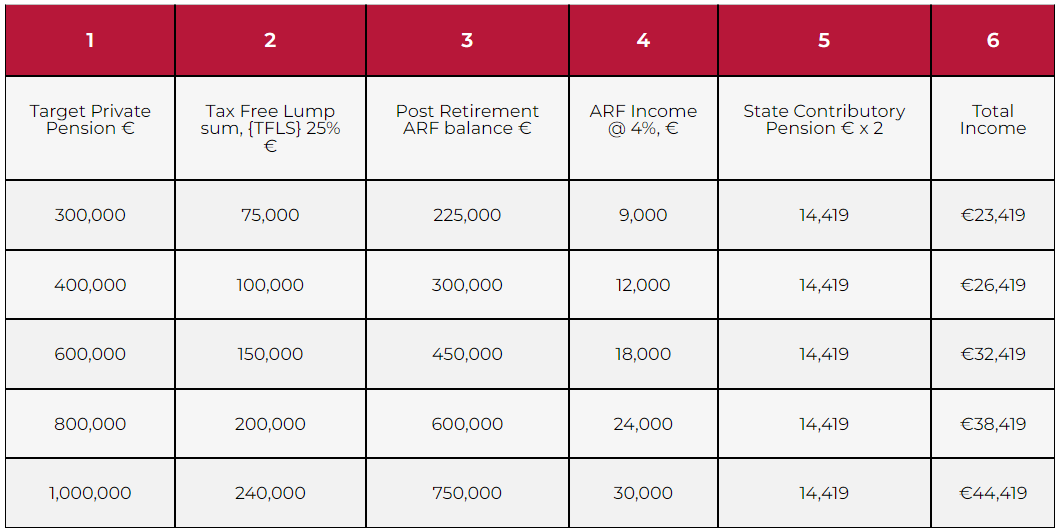

Single (incl. the State Contributory Pension)

| 1 | 2 | 3 | 4 | 5 | 6 |

|---|---|---|---|---|---|

|

Target Private Pension € |

Tax Free Lump sum, {TFLS} 25%

€

|

Post Retirement ARF balance € |

ARF Income @ 4%, € |

State Contributory Pension € x 2 |

Total Income |

|

300,000 |

75,000 |

225,000 |

9,000 |

14,419 |

€23,419 |

|

400,000 |

100,000 |

300,000 |

12,000 |

14,419 |

€26,419 |

|

600,000 |

150,000 |

450,000 |

18,000 |

14,419 |

€32,419 |

|

800,000 |

200,000 |

600,000 |

24,000 |

14,419 |

€38,419 |

|

1,000,000 |

240,000 |

750,000 |

30,000 |

14,419 |

€44,419 |

Assumptions:

- Everyone qualifies for the max. State Pension (circa 40 yrs. social insurance)

- At retirement the couple/ individual chooses the Approved Retirement Fund (‘ARF’) option, not an annuity.

So, what can each of us do to improve our chances of comfortably reaching our target Private Pension Income level?

The good news is that the Target Private Pension levels shown are attainable by many pension holders whether they are an employee, self-employed or a business owner. Pension plans are very tax effective for everyone, but as with any plan it does require regular review and engagement to achieve the long-term goals. This review should include the following.

- Arrange an annual meeting with your Financial Adviser, to review performance of your funds versus average market returns and versus its peer group (most FA’s have this detail) and any potential tweaks to achieve your long term goals. You should also discuss your target retirement fund level and the level of tax you might expect to pay in retirement.

- Don’t be fixated on your manager’s short-term performance (1 Year), instead focus on their performance over the 3-, 5- and 10-year period as these are better indicators of their ability to manage through the economic cycles. It can sometimes be a case of short term pain for long term gain.

- Do you have a handle on your plan’s total charges? This should include direct and indirect charges, aka ‘the total expense ratio’ (TER ratio), although the TER is informative it needs to be weighed up against the managers investment performance.

- Is your Financial Adviser and/ the Pension Manager giving you a satisfactory service level and a prompt response to your queries, this is important as most plans have an annual Advisory fee.

- If you are a member of a Group/company scheme, this can mean you benefit from lower all-in management charges versus individual pension plans, but often Group plans have a lower range of Pension Investment Funds than individual pension plans. They key is to find a balance with a low cost and a decent fund range.

- If you are playing pension catch up (starting late), make sure that you are maximizing your annual Revenue Pension contribution rate. For a 50-year-old this equates to an annual contribution of up to 30% of annual Salary and rises to 40% for a 60-year-old.

- If you are self-employed or a business owner and have excess reserves, speak to your Financial Adviser on setting up a tax efficient pension plan (PRSA) that your business (Employer) can make material annual contributions to if you are a company owner, partnership, or a sole trader.

Switch Fund Manager

If after conducting your annual review you assess that your pension is under-performing then it is time to act, speak to an Independent Certified Financial Planner who will advise you on the most appropriate options and find the most suitable manager for your needs. It’s never too late to seek independent advice to get your plan back on track. It’s better when your planner is working on behalf of you and not an insurance or investment company.

If what you have read resonates with you and you are ready to take the next step,

Should you have any questions on this or any other aspects relating to taking a ‘hands-on approach’ to your pension, please get in touch to arrange a consultation with one of our financial experts here at Imperius Wealth and we will be happy to guide you through the possibilities.

Just fill out the form below and one of our Expert Financial Planners will be in touch:

Subscribe to our quarterly newsletter.

By submitting this form, you agree to receive emails from Imperius Wealth. You may unsubscribe from these communications at any time. For information on how to unsubscribe, as well as our privacy practices and commitment to protecting your privacy, please review our Privacy Policy.