What is an Executive Pension (EP)?

It is a tax-exempt Revenue approved Pension vehicle that allows business owners and key employees to get the most value from their pension contributions. It allows a business owner to transfer surplus profits from the company to his/her Executive Pensions plan with no liability to Benefit-in-Kind.

Why?

It is a very flexible means of building a retirement pot suitable for a business owner or senior employees.

- Business owner who may want to ‘catch’ up on his Pension contributions.

- Back-funding is a flexible feature which allows the EP owner to potentially back-fund for years where he was in salaried service but not pensioned.

- If the company makes the payments to the business owners Executive Pensions plan, contributions are paid gross with no BIK liability

- The Company gets corporation tax relief on the employer contributions in the year made

Process – How to qualify for an Executive Pensions Ireland

| Requirements | Benefits |

| Limited company status | Employer can make generous contributions -which are not restricted by age related limits but are linked to salary, age, and years to retirement |

| Business owner or key employee must have Schedule E Income | 40% tax relief on any personal contributions |

| Availability of excess company profits | No Personal tax liability for the EP owner, any investment growth is tax free |

| Must be set-up in a trust | Flexible can decide each year on contribution level and can stop and re-start as suits employer |

Executive Pension - Maximum annual contributions levels

Maximum Executive Pension Contribution Levels -

Example

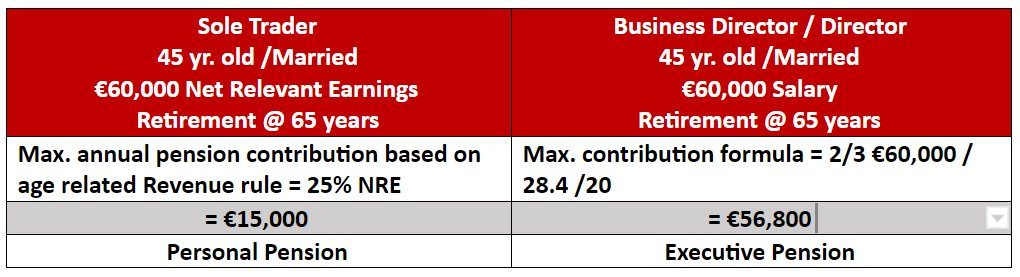

Max. Contribution limit = 2/3 Salary *Capitalisation factor less Retained Pension / yrs. to retire

Cap. Factor is higher for a male with a spouse or civil partner.

An Earnings cap of €115,000 applies to contributions.

Advantages of an Executive Pension for Business Owner ‘Versus’ Sole Trader Personal Pension

Taxation Pensions – at Retirement

The maximum individual pension benefit in Ireland is €2 million known as the Standard Fund Threshold

Individual with a retirement pot of €2 million, would receive a tax-free lump sum of €440k on €500k of benefits drawdown.

An individual who accumulates Pension Benefits greater €2 million will pay tax of 40% on all these pensions assets more than €2 million

Summary

There’s a lot of moving parts when it comes to retirement planning while running a business. If you’d like to hear the full list of the options available to you, please contact me and I would be happy to schedule a time for a 15 min. chat about your goals and how I can help you achieve them.