How I’d set up my Pension if I was a Company Director at 48 (and why now is not too late).

A while back, I was chatting to a friend at the bar, he’s 48, runs his own limited company, business is flying, but he leans in and says:

“To be honest, I’ve done nothing about a pension. Is it too late to sort it out?”

It’s a question I’ve heard more than once, and if you’re a company director with profits building up in the business, it might sound familiar.

Here’s what I’d do if I were in your shoes.

- Route 1: OMA Executive Pension

This one’s the game changer. It lets your company make large, tax-deductible contributions, even for years you didn’t pay into a pension. If you’re looking to catch up and make a real dent in your retirement planning, this is your best bet.

- Route 2: Advice PRSA

A solid option, but a bit more limited. Your company can typically only contribute 1x your salary per year. Still useful, but not as powerful if you’re trying to make up for lost time.

The feeling?

Once directors see how much they can transfer from company profits into their own future pension, and reduce tax while doing it, there’s a genuine sense of relief. Like, “why didn’t I do this sooner?”

If you’re in a similar boat, we’ve put together a quick visual comparing both options.

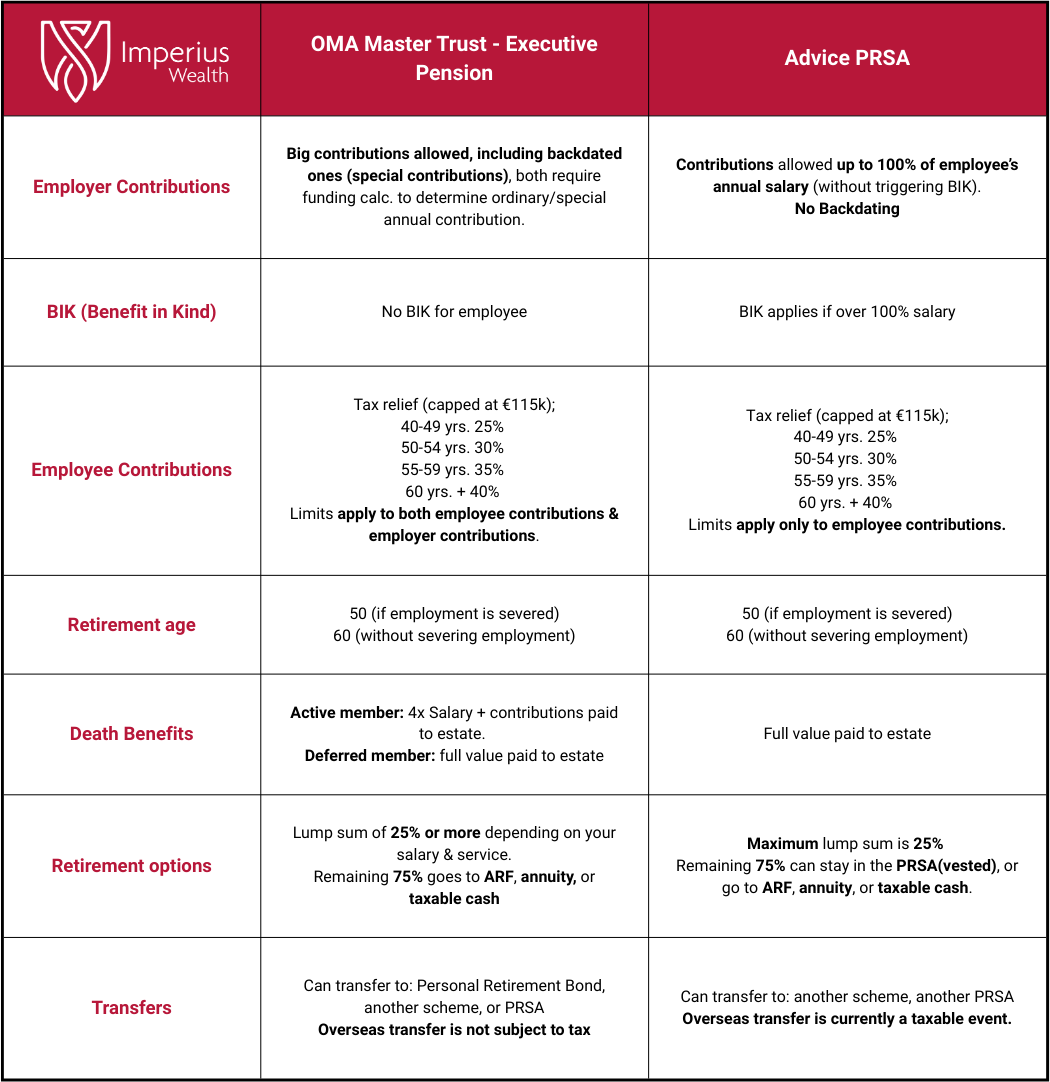

Company Director Pension Options

| OMA Master Trust - Executive Pension | Advice PRSA | |

|---|---|---|

|

Employer Contributions |

Big contributions allowed, including backdated ones (special contributions), both require funding calc. to determine ordinary/special annual contribution. |

Contributions allowed up to 100% of employee’s annual salary (without triggering BIK). No Backdating |

|

BIK (Benefit in Kind) |

No BIK for employee |

BIK applies if over 100% Salary |

|

Employee Contributions |

Tax relief (capped at €115k);

40-49 yrs. 25%

50-54 yrs. 30%

55-59 yrs. 35%

60 yrs. + 40%

Limits apply to both employee contributions & employer contributions. |

Tax relief (capped at €115k); 40-49 yrs. 25% 50-54 yrs. 30% 55-59 yrs. 35% 60 yrs. + 40% Limits apply only to employee contributions. |

|

Retirement Age |

50 (if employment is severed)

60 (without severing employment) |

50 (if employment is severed) 60 (without severing employment) |

|

Death Benefits |

Active member: 4x Salary + contributions paid to estate.

Deferred member: full value paid to estate |

Full value paid to estate |

|

Retirement Options |

Lump sum of 25% or more depending on your salary & service.

Remaining 75% goes to ARF, annuity, or taxable cash |

Maximum lump sum is 25% Remaining 75% can stay in the PRSA(vested), or go to ARF, annuity, or taxable cash. |

|

Transfers |

Can transfer to: Personal Retirement Bond, another scheme, or PRSA

Overseas transfer is not subject to tax |

Can transfer to: another scheme, another PRSA Overseas transfer is currently a taxable event. |

If you would find above information relavant and would like to discuss further, please contact one of our financial advisers at hello@imperiuswealth.com to arrange a callback.

Subscribe to our quarterly newsletter.

By submitting this form, you agree to receive emails from Imperius Wealth. You may unsubscribe from these communications at any time. For information on how to unsubscribe, as well as our privacy practices and commitment to protecting your privacy, please review our Privacy Policy.